Here’s what you need to know:

The Bank of England’s new head, Andrew Bailey, said Friday that his central bank was “not out of firepower,” noting that it could cut interest rates below zero if necessary.

Mr. Bailey, who started his job in March and was delivering a speech at the Kansas City Fed’s virtual Jackson Hole symposium, underlined that he and his colleagues saw negative rates as a possible tool to stoke economic growth at a time when interest rates were already at very low levels across advanced economies.

The central bank has “made clear that our box does include other tools, including the possibility of negative rates,” Mr. Bailey said. “We are not out of firepower by any means, and to be honest it looks from today’s vantage point that we were too cautious about our remaining firepower” before the coronavirus pandemic.

Global central banks including the Bank of Japan and the European Central Bank have cut interest rates below zero, which are meant to discourage banks from stashing their cash at central banks and instead push them to lend more. Fed officials, on the other hand, have regularly ruled such a policy out. They say they doubt whether such tools are effective, and do not think that they would work well in the United States.

Mr. Bailey first indicated earlier this month that negative interest rates could be a possibility in the United Kingdom.

President Trump has at times called for negative rates in the United States, pointing out that other central banks have lowered borrowing costs below zero and arguing that America’s reticence to do so puts it at a competitive disadvantage.

The Fed sets its policies independently of the White House.

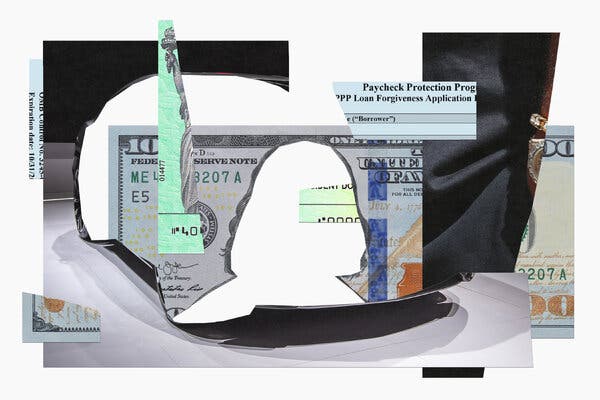

Investigators have charged big spenders with cheating the Paycheck Protection Program for small businesses. But more fraud lies below the surface, and it’ll be harder to find.

The Justice Department has made at least 41 criminal complaints in federal court against nearly 60 people, who collectively took $62 million from the P.P.P., the federal government’s signature coronavirus relief program for small businesses, by using what law enforcement officials said were forged documents, stolen identities and false certifications.

The criminal complaints read like catalogs of luxury bling: a diamond-laden $52,000 Rolex, a gambling spree at the Bellagio, two Lamborghinis, a pair of Cadillac Escalades, a Rolls-Royce.

They are just “the smallest, tiniest piece of the tip of the iceberg,” said Hannibal Ware, the inspector general of the Small Business Administration, which led the program.

But with their ostentatious spending and clearly faked records, those alleged thefts have also been the easiest to spot.

The relief program, a centerpiece of the CARES Act, poured $525 billion into the economy in just four months before coming to an end. More than five million businesses received loans, which could be forgiven if used for payroll and certain other expenses. Now, that hastily created and frequently chaotic program is entering its next messy stage, one that lenders and government officials expect to take years: the hunt to recapture illicitly obtained cash.

The challenge facing scores of state and federal agencies is enormous. The S.B.A.’s fraud hotline, which received fewer than 800 calls last year, has already had 42,000 reports about coronavirus-linked graft.

Stocks rose on Wall Street in early trading Friday. The S&P 500 — now in record territory — was on track for its seventh consecutive daily gain, and the Dow Jones industrial average was on the cusp of breaking even for the year.

Outside of the U.S., Japanese shares were roiled by news that Japan’s prime minister, Shinzo Abe, would step down because of ill health. Tokyo’s Nikkei, which had been in positive territory before the announcement about Mr. Abe, finished 1.4 percent lower.

Mr. Abe’s decision to step down as Japan’s longest-serving prime minister could mark the end of “Abenomics,” his combination of monetary easing, fiscal stimulation and corporate reform. The policies restored some economic health to Japan, but its promises of change in the corporate world — including efforts to empower women, reduce the influence of nepotism and change entrenched work culture — remained unfulfilled.

U.S. consumer spending rose 1.9 percent in July, the Commerce Department said Friday, beating analyst expectations and offering a glimmer of hope for an economic recovery after the devastation of the pandemic. July’s gain is the third straight month of increases in consumer spending. But crucial $600-a-week jobless payments which expired at the end of that month may impact August’s recovery.

The Fed chair, Jerome H. Powell, said Thursday that the central bank would continue to stimulate the economy even if inflation briefly rises above the target level of 2 percent. The change in tactics suggested interest rates would remain low. The news caused turbulence in the markets, but the S&P 500 ended the session up 0.17 percent at another record high.

The editors and reporters for the DealBook newsletter sift through a lot of company reports and listen to many earnings conference calls. These are some of the things that caught our notice this week:

📈 “This quarter really is a victory for stakeholder capitalism.” — Marc Benioff, the Salesforce chief executive, about earnings that led to the company’s biggest ever one-day stock gain

😷 “We sold about $130 million in masks in Q2 through compelling consumer marketing and digital storytelling that has us ranked as the No. 1 Google search results for ‘face mask style guide.’” — Sonia Syngal, Gap’s chief executive.

🍳 “We are excited about the growing interest in cooking, especially for millennials.” — Laura Alber, the Williams-Sonoma chief executive.

🏠 “With a long-term increase in remote working, many people are now choosing to live where they want rather than where their job previously required.” — Douglas Yearley, Toll Brothers’ chief executive.

🧳 “The only category that comped negative was our luggage department, which makes 100 percent sense with no one traveling.” — John Swygert, the Ollie’s Bargain Outlet chief executive.

🐸 “We introduced what could be the top toy of the year, Baby Yoda, and sold tens of thousands in a matter of days.” — Michael Witynski, Dollar Tree’s chief executive.

🐶 “We are seeing the pet category perform largely as it normally does. … Pets always eat at home, so the increase from stay-at-home consumption is largely focused on humans.” — Mark Smucker, the chief executive of J.M. Smucker.

The British government has a new message to deliver: It’s safe to return to work.

Starting next week, when schools reopen, the government will begin an ad campaign designed to reassure people that their workplaces have been made safe over the summer and they can return to them with the right health and safety precautions.

“Next week we will showcase the benefits of returning safely to work and raise awareness of companies getting this right,” a government spokesperson said.

The advertisements, to be placed mainly in local and regional media, come amid mounting concern from some business groups that prolonged working from home is seriously harming the economies of town and city centers that rely on commuters.

But many companies don’t want to be seen to be pressuring their employees to return. Recently the British asset management firm Schroders (with about 3,000 employees in Britain) said it would permanently allow flexible working, and the trading company IG (about 750 employees) said none of its staff would be required to return this year, though its office would reopen on Sept. 7.

Across all industries, 40 percent of people said they were working remotely, according to a survey earlier this month by the Office for National Statistics. But in certain sectors — including education, communications and legal services — the share of people working from home jumped to more than three-quarters.

Carolyn Fairbairn, head of the Confederation of British Industry, said that getting people back into offices and workplaces was as essential to the economy as schools reopening. “The costs of office closure are becoming clearer by the day,” she wrote in op-ed published in The Daily Mail on Thursday. “Some of our busiest city centers resemble ghost towns, missing the usual bustle of passing trade.”

Coca-Cola said Friday that it would cut jobs as it restructured its business. Though the company did not specify how many jobs would be lost, it said it would offer voluntary separation packages to 4,000 workers in the United States, Canada and Puerto Rico, and a similar package to international workers. Coca-Cola said the severances were expected to cost the company $350 million to $550 million.

MGM Resorts International said on Friday that it was laying off 18,000 U.S. employees who were furloughed in March after the pandemic struck. In a letter to employees, the chief executive Bill Hornbuckle said MGM would continue to provide health benefits to furloughed employees through Sept. 30. Many of MGM’s properties on the Vegas strip have reopened with limited capacity because of virus restrictions. MGM’s Empire City in New York state and the Park MGM in Las Vegas remain closed. At the beginning of this year, MGM Resorts employed 70,000 people in the United States.

The only Gap Inc. brand to post a sales increase in the second quarter was Athleta, its athleisure chain, while its worst drop was at the office garb-focused Banana Republic, which saw its business halved. Gap, which also owns Old Navy and its namesake chain, reported an 18 percent sales decline to $3.3 billion for the three months ended Aug. 1 and a net loss of $62 million. Gap said on its earnings call that it sold $130 million in face masks during the quarter and secured the No. 1 Google search result for “face mask style guide.”

The Federal Reserve, in a significant shift that could keep interest rates low for longer periods, said it would focus on keeping unemployment low and allow inflation to run slightly higher in good times. The Fed chair, Jerome H. Powell, announced the change in a speech on Thursday at the Kansas City Fed’s annual Jackson Hole symposium

Lord & Taylor said on Thursday that it was starting liquidation sales at its 38 stores and website after filing for bankruptcy earlier this month and failing to find a buyer. The retailer is owned by the clothing rental start-up Le Tote, which purchased Lord & Taylor in an unusual $100 million deal last year. The companies sought Chapter 11 bankruptcy protection on Aug. 2, saying that they were already under pressure before the pandemic “greatly compounded” their challenges

The White House wants the Treasury Department to ensure that companies, not workers, will be held liable for paying the employee portion of the payroll tax when President Trump’s tax holiday ends.

The Treasury Department has not been willing to issue such guidance, though it is unclear why. Businesses, which have been fielding questions from their employees about when the tax cuts will begin, would prefer that Congress legislate any changes to tax policy. It is also not clear that the White House would have the legal authority to shift the tax burden in such a manner.

The president’s executive order suspends payments, but employees will be on the hook to pay the deferred taxes back when the tax holiday ends. Many companies are expected to opt out of participating to avoid sticking their employees with a giant bill next year.

The dispute between the White House and the Treasury Department over the guidance was reported earlier by Bloomberg News. A department spokeswoman declined to comment. Judd Deere, a White House spokesman, did not dispute that the Trump administration wanted companies to be liable for the tax but said he would not comment on internal policy deliberations.

The payroll tax suspension plan has been fraught from the beginning. Treasury Secretary Steven Mnuchin was skeptical of the idea and has said participation would be optional. Mr. Trump has said that he will push Congress to make the tax deferral permanent if he is re-elected, but if Democrats retain control of the House of Representatives, more tax cuts are unlikely.

A new kind of corporate consultant has emerged. Their larger goal is to soften cruel capitalism, making space for the soul, and to encourage employees to ask if what they are doing is good in a higher sense, reports Nellie Bowles.

Before the pandemic, these agencies got their footing helping companies with design — refining their products, physical spaces and branding. They also consulted on strategy, workflow and staff management. With digital workers stuck at home since March, a new opportunity has emerged. Employers are finding their workers atomized and agitated, and are looking for guidance to bring them back together. Now the sacred consultants are helping to usher in new rituals for shapeless workdays, and trying to give employees routines that are imbued with meaning.

Ezra Bookman founded Ritualist, which describes itself as “a boutique consultancy transforming companies and communities through the art of ritual,” last year in Brooklyn. He has come up with rituals for small firms for events like the successful completion of a project — or, if one fails, a funeral.

“How do we help people process the grief when a project fails and help them to move on from it?” Mr. Bookman said.

Messages on the start-up’s Instagram feed read like a kind of menu for companies who want to buy operational rites a la carte: “A ritual for purchasing your domain name (aka your little plot of virtual land up in the clouds).” “A ritual for when you get the email from LegalZoom that you’ve been officially registered as an LLC.”

Related reporting

More World News →

Paul Biya’s Re-Election: What Cameroon’s Political Longevity Reveals About Leadership and Governance in Africa

From Power to Prison: The Fall of France’s Former President Nicolas Sarkozy

The War in Ukraine: A Comprehensive Analysis of the Conflict