Daily Business Briefing

Sept. 8, 2021UpdatedSept. 8, 2021, 4:03 p.m. ET

Sept. 8, 2021, 4:03 p.m. ET

WASHINGTON — The United States could default on its debt sometime in October if Congress does not take action to raise or suspend the debt limit, Treasury Secretary Janet L. Yellen warned on Wednesday.

The “extraordinary measures” that the Treasury Department has been employing to finance the government on a temporary basis since Aug. 1 will be exhausted next month, Ms. Yellen said in a letter to lawmakers. She added that the exact timing remained unclear but that time to avert an economic catastrophe was running out.

“Once all available measures and cash on hand are fully exhausted, the United States of America would be unable to meet its obligations for the first time in our history,” Ms. Yellen wrote.

To delay a default, Treasury has in the last month suspended investments in the Civil Service Retirement and Disability Fund, the Postal Service Retiree Health Benefits Fund and the Government Securities Investment Fund of the Federal Employees Retirement System Thrift Savings Plan.

The distribution of pandemic relief payments this year and uncertainty over incoming tax payments this month have made it more challenging than usual to predict when funds will run out. Ms. Yellen said that a default would cause “irreparable harm” to the U.S. economy and to global financial markets and that even coming close to defaulting could be harmful.

“We have learned from past debt limit impasses that waiting until the last minute to suspend or increase the debt limit can cause serious harm to business and consumer confidence, raise short-term borrowing costs for taxpayers and negatively impact the credit rating of the United States,” she wrote.

Democratic leaders have been insisting for months that Republicans join them in raising the debt ceiling, saying the government hit its last debt limit because of the spending and tax cutting of the Trump administration, what Speaker Nancy Pelosi of California on Wednesday called “the Trump credit card.”

But Senator Mitch McConnell of Kentucky, the Republican leader, has been just as emphatic that he will keep Senate Republicans from helping Democrats on the issue. Democrats may try to attach the increase to measures such as an emergency spending bill to pay for relief and reconstruction after Hurricane Ida, wildfires and heat waves from the summer — daring senators from Louisiana and Western states to vote no.

The showdown has again put the parties into a game of chicken, with a debt default and potential economic crisis as the consequence.

Ms. Pelosi, at her weekly news conference on Wednesday, said emphatically that Democrats would not include a statutory increase in the government’s borrowing authority in a budget bill being drafted this month. That bill, under complicated budget rules, could pass without Republican votes in the Senate.

Instead, Democratic leaders will dare Senate Republicans to filibuster a bill that does raise the debt ceiling.

“We Democrats supported lifting the debt ceiling” during the Trump administration, she said, “because it was the responsible thing to do.” She added, “I would hope that the Republicans would act in a similarly responsible way.”

Democrats have several options they are considering. The government will run out of operating funds at the end of the month, so a debt ceiling increase could be attached to a stopgap spending measure — meaning a Republican filibuster would not only jeopardize the government’s full faith and credit, it could shut down the government.

Democrats could also attach it to a major infrastructure bill that passed the Senate with bipartisan support and is supposed to get a House vote by Sept. 27.

Read more

WASHINGTON — The wealthiest 1 percent of Americans are the nation’s most egregious tax evaders, failing to pay as much as $163 billion in owed taxes per year, according to a Treasury Department report released on Wednesday.

The analysis comes as the Biden administration pushes lawmakers to embrace its ambitious proposal to beef up the Internal Revenue Service to narrow the “tax gap,” which it estimates amounts to $7 trillion in unpaid taxes over a decade. The White House has proposed investing $80 billion in the agency over the next 10 years to hire more enforcement staff, overhaul its technology and usher in new information-reporting requirements that would give the government greater insight into tax evasion schemes.

The proposals have been met with deep skepticism from Republicans and business lobbyists who argue that the I.R.S. cannot be trusted with more power and that the proposals are an invasion of privacy.

Democrats are counting on raising money by collecting more unpaid taxes to help pay for the $3.5 trillion spending package they are drafting. On Thursday, the House Ways and Means Committee is set to begin formally drafting its voluminous piece of the 10-year measure to combat climate change and reweave the nation’s social safety net, with paid family and medical leave, expanded public education, new Medicare benefits and more.

The Treasury Department estimates that its tax gap proposals could raise $700 billion over a decade.

The department’s report, which was written by Natasha Sarin, deputy assistant secretary for microeconomics, makes the case that narrowing the tax gap is part of the Biden administration’s ambition to create a more equitable economy, as audits and enforcement actions will be aimed at the rich.

“For the I.R.S. to appropriately enforce the tax laws against high earners and large corporations, it needs funding to hire and train revenue agents who can decipher their thousands of pages of sophisticated tax filings,” Ms. Sarin wrote. “It also needs access to information about opaque income streams — like proprietorship and partnership income — that accrue disproportionately to high earners.”

The report combines academic research on how the tax gap has historically been distributed across the income scale with 2019 tax data.

Tax compliance rates are high for low- and middle-income workers who have their taxes deducted automatically from their paychecks. The rich, however, are able to use accounting loopholes to shield their tax liabilities.

The Biden administration has pledged that individuals with “actual income” less than $400,000 per year will not see their audit rates go up.

A Congressional Budget Office report last week found that expanding the enforcement capacity of the I.R.S. would not raise as much money as the Treasury Department projects. The analysis, which did not include the information reporting part of the tax gap plan, estimated that the additional enforcement funds would raise $200 billion over a decade, while the Treasury Department projected it would raise about $320 billion over that time.

Read more

Participants in the Macy’s Thanksgiving Day Parade must be masked and vaccinated, with a few exceptions, the company said on Wednesday, as the annual tradition plans a return to a version of its old self this November after a muted performance last year.

The announcement is the latest sign that New York is determined to resume some semblance of normalcy even as it grapples with the spread of the highly contagious Delta variant of the coronavirus.

Macy’s said its 95th celebration would travel a longer route than the one block it was confined to in 2020 and bring in marching bands and other groups that were unable to perform last year. It will allow 80 to 100 handlers for its giant character balloons after reducing the number last year.

The company said that it anticipated thousands of participants again, though fewer than its typical 8,000, and that all volunteer participants and staff must be fully vaccinated. They must also wear face coverings, with some exceptions for performers, and maintain social distancing throughout much of the event.

The pandemic upended traditions including festivals and Santa Claus meetings last year, and the parade became largely a television event as many spectators were told to stay home and the parade route shrank from its usual two-mile stretch. Some balloons even had flights that were pretaped for broadcast. A representative for Macy’s said the company was still determining this year’s route but expected that it would be closer to two miles.

“We applaud Macy’s work to creatively continue this beloved tradition last year,” Mayor Bill de Blasio said in a statement, “and look forward to welcoming back parade watchers to experience it safely, live and in person this November.”

Opening statements in the case of Elizabeth Holmes, the founder of the blood testing start-up Theranos, began in San Jose, Calif., on Wednesday morning, kicking off one of Silicon Valley’s most anticipated trials.

“This is a case about fraud and about lying and cheating to get money,” said Robert Leach, an assistant U.S. attorney for the Northern District of California, who is leading the prosecution for the government.

Ms. Holmes, 37, has been charged with 12 counts of wire fraud and conspiracy to commit wire fraud in connection with money she raised for Theranos, which dissolved in 2018 after its blood tests were revealed to have problems.

Lance Wade, Ms. Holmes’s lawyer, painted a dramatic picture of a passionate entrepreneur who may have failed but was not a criminal.

“Elizabeth Holmes,” Mr. Wade said in his opening statement, pausing for effect, “worked herself to the bone for 15 years trying to make lab testing cheaper and more accessible.”

“The villain the government just presented is actually a living breathing human being who did her very best each and every day,” he added.

A jury will decide whether Ms. Holmes, who founded Theranos in 2003 and hawked a mission of revolutionizing health care, lied to investors about her company’s technology.

Ms. Holmes claimed Theranos’s machines, called Edison, could quickly conduct a wide range of blood tests using just a drop of blood. The United States has accused Ms. Holmes of knowing that the tests were limited and unreliable, harming patients who used them. Prosecutors also said she overstated Theranos’s business deals and performance.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

Erin Woo📍Reporting from San Jose, Calif.Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

Elizabeth Holmes, the disgraced founder of the blood testing start-up Theranos, stands trial for two counts of conspiracy to commit wire fraud and 10 counts of wire fraud.

Here are some of the key figures in the case →

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

Holmes founded Theranos in 2003 as a 19-year-old Stanford dropout. She raised $700 million from investors and was crowned the world’s youngest billionaire, but has been accused of lying about how well Theranos’s technology worked. She has pleaded not guilty.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

Ramesh Balwani, known as Sunny, was Theranos’s president and chief operating officer from 2009 through 2016 and was in a romantic relationship with Holmes. He has also been accused of fraud and may stand trial next year. He has pleaded not guilty.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

David Boies, a prominent litigator, represented Theranos as its lawyer and served on its board.

He tried to shut down whistle-blowers and reporters who questioned the company’s business practices.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

The journalist John Carreyrou wrote stories exposing fraudulent practices at Theranos.

His coverage for The Wall Street Journal helped lead to the implosion of Theranos.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

Tyler Shultz and Erika Cheung are former Theranos employees and were whistle-blowers. They worked at the start-up in 2013 and 2014.

Shultz is a grandson of George Shultz, a former secretary of state who was on the Theranos board.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.

James Mattis, a retired four-star general, was a member of Theranos’s board.

He went on to serve as President Donald J. Trump’s secretary of defense.

Who’s Who in the Elizabeth Holmes Trial

Erin Woo📍Reporting from San Jose, Calif.Edward Davila, a federal judge for the Northern District of California, will oversee the case.

Kevin Downey, a partner at the Washington law firm Williams & Connolly, is the lead lawyer for Holmes.

Robert Leach, an assistant United States attorney for the Northern District of California, will lead the prosecution for the government, along with other prosecutors from the U.S. attorney’s office.

Read more about Elizabeth Holmes:

Aug. 30, 2021Item 1 of 9

Theranos’s former president, Ramesh Balwani, known as Sunny, is being tried in a separate case set to begin next year. Both Ms. Holmes and Mr. Balwani have pleaded not guilty. Judge Edward Davila of the U.S. District Court for the Northern District of California is presiding over the cases.

If convicted, Ms. Holmes could face up to 20 years in jail, which would make her one of the few Silicon Valley executives accused of wrongdoing to go to jail.

The trial caps years of delays and legal squabbles over things like which emails and arguments can be used and whether Ms. Holmes should be required to wear a mask while sitting in the courtroom.

Last week, a jury of seven men and five women was sworn in after the elimination of many potential jurors who had either heard of Ms. Holmes, had direct experience with domestic abuse or had schedules that could not accommodate the three-month trial.

Ms. Holmes’s lawyers have indicated that they may use a mental health defense, arguing that Mr. Balwani, whom she dated, was emotionally and physically abusive. Mr. Balwani has denied the accusations. Ms. Holmes’s lawyers have also indicated in court filings that she is likely to take the stand.

In court documents filed over the weekend, prosecutors listed more than 200 potential witnesses including David Boies, Theranos’s former lawyer; Henry Kissinger, the former secretary of state who sat on Theranos’s board; James Mattis, the former defense secretary and a Theranos director; and Rupert Murdoch, the media mogul, who backed Theranos and was part of a lawsuit over its demise. Some names were displayed as initials.

Ms. Holmes’s lawyers listed more than 60 witnesses, including several of the U.S. attorneys on the case; John Carreyrou, a reporter and the author of a book about Theranos; William Frist, the former U.S. Senator who sat on the Theranos board; and Ms. Holmes.

In a separate filing, lawyers for Ms. Holmes also asked that testimony from three former Theranos employees be excluded. One of the witnesses, Erika Cheung, worked in Theranos’s lab and reported problems with its blood testing to federal regulators. Ms. Holmes’s lawyers argued that various parts of Ms. Cheung’s testimony would be irrelevant, based on hearsay or not directly connected to Ms. Holmes.

Ms. Holmes’s lawyers also asked to exclude testimony from Daniel Edlin, a former project manager at the company, and Danise Yam, Theranos’s corporate controller for 11 years.

Prosecutors responded with exhibits backing up Ms. Cheung’s claims. On Tuesday, Judge Davila ordered that such an exclusion would be “premature” ahead of hearing the government’s questions or argument.

Read more

Cascade Investment, the firm that manages the fortune of Bill Gates, is buying half of a Saudi billionaire’s stake in Four Seasons for $2.2 billion — making Mr. Gates the majority owner of the luxury hotel chain.

The deal was announced on Wednesday morning by Cascade and Kingdom Holding, the investment firm of the Saudi billionaire, Prince Alwaleed bin Talal, in Riyadh. Mr. Gates’s stake in Four Seasons will increase to about 71 percent, from a little less than 50 percent.

The transaction comes on the heels of Mr. Gates’s divorce last month from Melinda French Gates, the Microsoft founder’s wife of nearly three decades. Few details of their division of cash and assets as part of the divorce are known. But Cascade continues to manage much of the Gates fortune, as well as the endowment of the Gates Foundation, the charity the former couple co-founded in 2000.

Cascade first teamed up with Kingdom to buy a position in the Four Seasons in 2007, when each acquired a 47.5 percent stake for a total price of $3.8 billion. The remaining 5 percent is held by Isadore Sharp, the founder of Four Seasons.

In 2019, before the pandemic hit, Cascade and Kingdom discussed the idea of taking Four Seasons public. More recently, the two companies also discussed the idea of selling down one or both of their stakes, two people familiar with the matter said in May, but ultimately, Cascade chose to stay put.

The hospitality sector has been hard hit by the pandemic. Despite an increase in leisure travel after vaccinations became widely available this year, a survey in mid-August commissioned by the American Hotel & Lodging Association indicated that amid a resurgence in cases in the United States, 42 percent of the 2,200 respondents were canceling travel plans, with no intention to reschedule.

Coinbase, the largest cryptocurrency exchange in the United States, said on Wednesday that federal securities regulators were threatening to sue it over a proposed financial product that would let customers earn interest on digital asset deposits.

The company, in a regulatory filing, said the Securities and Exchange Commission notified it on Sept. 1 that its Lend product could violate securities laws. Regulators, the company said, might respond to Lend’s release by seeking a civil injunction.

The issue raised by Lend — an interest-generating service that somewhat resembles accounts traditionally offered by banks — is whether it will be engaged in trading or offering products to consumers that are considered securities, which the S.E.C. has the power to regulate.

The warning to Coinbase, which listed on the public market in April, is an indication that the S.E.C. is closely watching cryptocurrency companies — especially as they move into the territory of heavily regulated industries, such as banking. Gary Gensler, the S.E.C. chair, has said he is worried about the effects that unregulated crypto exchanges and products could have on the markets and investors.

Lend, which Coinbase announced in June, would allow customers to earn interest on cryptocurrency deposits. Specifically, customers would be able to earn interest on USD Coin, a so-called stablecoin whose value is tied to the dollar. Yields would be higher than those offered on classic bank accounts, and Coinbase would be among numerous cryptocurrency businesses entering this sector.

Coinbase executives pushed back against the S.E.C. in online postings, saying that the Lend program doesn’t qualify as a security and that the commission’s notice caught them off guard.

“The S.E.C. has repeatedly asked our industry to ‘talk to us, come in.’ We did that here,” Coinbase’s chief legal officer, Paul Grewal, said in a blog post. “But today all we know is that we can either keep Lend off the market indefinitely without knowing why or we can be sued.”

Coinbase’s chief executive, Brian Armstrong, called the S.E.C. “sketchy” in an extensive thread on Twitter and said he went to Washington in May to meet with financial regulators at many agencies. “The S.E.C. was the only regulator that refused to meet with me,” he said.

By seeking permission to act, Mr. Armstrong said, Coinbase is facing more resistance from regulators than other cryptocurrency companies that have introduced similar products.

Securities lawyers were divided over the S.E.C.’s tactics in going after Coinbase. Daniel Hawke, an attorney with Arnold & Porter and a former chief of the S.E.C.’s market abuse division, said the agency’s trying to stop a product launch “sounds aggressive.”

But some legal experts said securities regulators appeared to be taking a somewhat cautious approach in giving Coinbase a fair warning of its thoughts as opposed to simply letting the company go forward with the lending product and then suing it later.

Tyler Gellasch, a former S.E.C. official who leads the nonprofit Healthy Markets Association, said the commission recognized the importance of carefully handling a new kind of product entering the market.

“This is a very large player in the cryptocurrency place, and they are extremely cautious in bringing down a hammer,” he said.

Coinbase is not the only company running into trouble with securities regulators over crypto-based interest-generating services. Officials in five states have targeted BlockFi, a cryptocurrency business that offers high yields on holdings. Zac Prince, BlockFi’s chief executive, said that the company was complying with the law but that regulators did not fully understand its offerings.

“Ultimately, we see this as an opportunity for BlockFi to help define the regulatory environment for our ecosystem,” he wrote in a note to customers.

Shares of Coinbase were down as much as 4 percent on Wednesday morning.

Read moreU.S. stocks fell in midday trading Wednesday, with the S&P 500 stretching its losses to a third consecutive day. The index ticked down 0.3 percent, while the Nasdaq composite was 0.7 percent lower.

The Labor Department said that job openings climbed for a fifth consecutive month in July. Job openings rose to 10.9 million in July from 10.2 million. The figures come after data on Friday showed August was one of the weakest months for hiring since the recovery began more than a year ago.

Cryptocurrencies prices continued to fall, with Bitcoin dropping to about $46,000, according to Coinbase, falling from as high as $52,500 earlier in the week. El Salvador adopted Bitcoin as legal tender on Tuesday, and the country faced a rocky start after its storage app was marred by technical glitches.

Coinbase stock fell as much as 4 percent after it said that the Securities and Exchange Commission had threatened to sue over a product that pays interest on cryptocurrency deposits. By midday it was down about 2.4 percent.

The yield on the benchmark 10-year Treasury note fell to 1.35 percent from 1.37 percent.

European stocks fell on Wednesday, with the Stoxx Europe 600 closing down 1.1 percent.

Canadian National’s bid to buy Kansas City Southern and create a rail network that stretches across North America is facing a new challenge, the DealBook newsletter reports.

TCI Fund Management, a longtime railroad investor, has started a proxy battle to oust Canadian National’s chief executive, Jean-Jacques Ruest. TCI wants Canadian National to stop pursuing the acquisition and overhaul its board.

“We believe CN’s best days are ahead of it, provided the company immediately withdraws from its reckless, irresponsible and value destructive pursuit of KCS,” the fund’s founder, Chris Hohn, said.

Canadian National has been duking it out with a smaller rival, Canadian Pacific, to buy Kansas City Southern. Canadian National has offered more money; Canadian Pacific, more deal certainty.

In May, Kansas City Southern went with Canadian National and its higher bid. But last week, the regulator that oversees rail deals, the Surface Transportation Board, ruled against the companies’ use of a voting trust, a common but controversial structure in such deals. Now, Kansas City Southern is back in talks with Canadian Pacific.

Canadian National’s bid “exposed a basic misunderstanding of the industry and the regulatory environment,” TCI argues.

The fight for Kansas City Southern is the first real test of guidelines put in place in 2001 to tighten scrutiny in deals that involve the largest railroads. The vote wasn’t even close: The Surface Transportation Board went against the trust 5 to 0.

Canadian Pacific, which has a proposed voting trust that regulators have not blocked, successfully argued for its deal with Kansas City Southern to be evaluated outside those guidelines, given its smaller size.

It has been clear from the Biden administration’s early days that it would be tough on deals. Still, the railroad industry earned a surprising spotlight in a sweeping executive order issued in July that focused on competition. And key voices, like Representative Peter A. DeFazio of Oregon, the Democratic chairman of the House Transportation Committee, have come out against a voting trust for the Canadian National deal.

TCI, though, has a hand in both pots. Along with its stake in Canadian National, TCI owns nearly 42 percent of Canadian Pacific, making the hedge fund the company’s largest shareholder, according to the market data firm Sentieo.

The size of TCI’s investment in Canadian National is slightly bigger than its Canadian Pacific stake — about $4.1 billion compared with roughly $4 billion, a person familiar with the investments said. Still, TCI’s dual investments raise questions about whether its efforts to stop the Canadian National deal also serve to strengthen its investment in Canadian Pacific.

A representative for Canadian National said the company “values input” from all of its shareholders and would continue to “make carefully considered decisions” in line with its priorities.

Read more

LOS ANGELES — In a June 2019 interview with Axios, Gov. Gavin Newsom of California, a Democrat who has long been seen as a friendly face to the technology industry, made a prediction: The state’s largest businesses were about to get “steamrolled” by federal regulators.

Back then, hammering Big Tech was in vogue among politicians from both parties, and Democrats had become particularly worried by the spread of misinformation on social media and the repeated mishandling of user data.

But those were simpler times, before a pandemic and a recall election that now threatens Mr. Newsom’s political career. Two years after those comments, the governor has backed away from his tech criticism and is instead focused on saving his job.

Mr. Newsom and the anti-recall effort have raised almost $70 million, about six times the pro-recall side, by courting some of the wealthiest individuals in California’s largest industry. Some in tech have even opened their pocketbooks while acknowledging that Mr. Newsom is not their ideal candidate.

Reed Hastings, Netflix’s chairman and co-chief executive, backed former Mayor Antonio Villaraigosa of Los Angeles, not Mr. Newsom, during the Democratic primary for governor in 2018. But Mr. Hastings has donated $3 million to oppose Mr. Newsom’s recall, saying Mr. Newsom at least provides “stability in leadership.”

“I have been impressed with his centrist thoughtful leadership, particularly on Covid,” Mr. Hastings said. “I’m not saying he hasn’t had missteps, but mostly symbolic ones, as opposed to substance.”

While it remains unclear what a Republican governor would mean for the industry — a successful recall would most likely mean that Larry Elder, the conservative radio host, would take office — many within the tech elite are hoping not to find out.

Ron Conway, a San Francisco venture capitalist who organized a March anti-recall letter that 75 tech luminaries signed, has more recently turned his efforts toward fund-raising for Mr. Newsom because of the “dire threat” he says a Republican governor could pose to California’s economic recovery and fight against Covid-19.

“I don’t know Larry Elder, but I know his positions — repealing mask and vaccine mandates, peddling conspiracy theories — he is in no way ready to be governor,” Mr. Conway said in an email interview. “The last thing the tech and business sectors want right now is more instability, chaos and uncertainty in California.”

Though some big names have spent money defending Mr. Newsom — Priscilla Chan, a doctor and the wife of Facebook’s chief executive, Mark Zuckerberg, gave $750,000, and Laurene Powell Jobs, the billionaire founder of the Emerson Collective and widow of Steve Jobs, has given $400,000 — others have been more reluctant. Yelp’s chief executive, Jeremy Stoppelman, who signed Mr. Conway’s anti-recall letter, has not given money, noting that “I haven’t been super involved, but I’ve been willing to say publicly recall is a bad idea.”

Although most tech leaders have sought stability during the pandemic, others have used their dissatisfaction with the governor’s crisis leadership as a jumping-off point. The venture capitalists David Sacks and Chamath Palihapitiya have previously been outspoken in their support of the recall, donating more than $100,000 each to the effort.

As it became clearer that Mr. Elder would most likely replace Mr. Newsom if the recall vote succeeded, Mr. Palihapitiya has cut back on public statements about the recall, while Mr. Sacks has continued his drumbeat of criticism. Representatives for Mr. Sacks and Mr. Palihapitiya declined requests for comment.

“Newsom is scaremongering about what happens if he gets recalled, but in truth, Democrats have a veto-proof majority in the Assembly and a new election is held in 14 months,” Mr. Sacks tweeted late last month. “So the only thing that happens is we send a strong message to the political class: do better.”

Others are hoping to avert Mr. Elder and what they see as potential chaos.

“It’s like Trump — it’s wild and unpredictable, and who knows what he stands for,” said Kim-Mai Cutler, a partner at Initialized Capital.

Read more

El Salvador faced a rocky transition in its adoption of Bitcoin as legal tender on Tuesday. The government’s app for facilitating transactions — its “digital wallet” — went offline temporarily, protesters took to the streets of the capital to denounce the move, and the price of Bitcoin dropped sharply, demonstrating the volatility of the cryptocurrency market.

President Nayib Bukele wrote on Twitter on Tuesday morning that the digital wallet, which is called Chivo after a slang word for “cool,” would be available to Salvadorans in the United States and almost anywhere in the world. But even as large companies such as McDonald’s began accepting Bitcoin payments in El Salvador, for a time the wallet was not available to anyone, and the country slowed its rollout.

Ford Motor said on Tuesday that it had hired the senior executive who was leading Apple’s secretive car project to help the automaker push further into electric vehicles.

The executive, Doug Field, will be responsible for turning Ford vehicles into software-driven products that can interact with customers and provide new types of services, something Ford and other car companies say will become more important.

At Apple, Mr. Field, 56, held the title of vice president of special projects and played an important role in a yearslong effort to develop an electric vehicle. His departure could be a blow to Apple’s auto ambitions, which have been a subject of intense speculation.

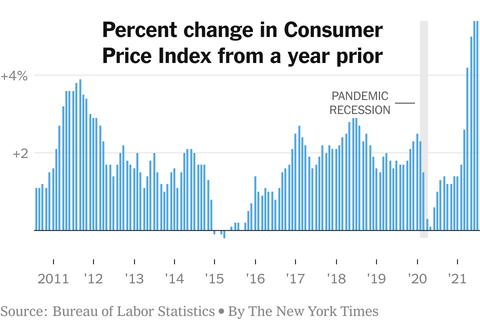

Price gains have become a source of annoyance among consumers and worry among policymakers who are concerned that rapid price gains might last. It is one of the main factors central bankers are looking at as they decide when — and how quickly — to return monetary policy to normal.

Prices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbers

Jeanna SmialekBreaking down the numbersPrices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbers

You may have noticed that you’re paying more for lots of things. Inflation has become a hot topic, but the question is whether it will last.

The items with the biggest increases may hold the answer →

Prices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbers

One area where costs have jumped: Products whose prices plunged at the onset of the pandemic.

Airfares and hotel prices, which dropped as demand evaporated in 2020, are rebounding. Airline tickets cost 19 percent more in July than a year earlier.

Prices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbers

Bikes, used cars and televisions are also costlier.

They include parts that are made overseas, like computer chips. With factories and shipping routes upended by the pandemic, these components are more expensive.

Prices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbers

Food is also more expensive. Prices at limited-service restaurants — places like Chipotle — were up 6.6 percent in the year through July.

Some of that might be tied to labor costs, as companies raise wages to attract workers.

Prices Are Going Up. Will It Last?

Jeanna SmialekBreaking down the numbersSo what does this mean for the future?

Categories showing big price gains are typically experiencing pandemic-related weirdness in one way or another. That’s why economists are pretty sure the current price pop will fade.

But as with all things pandemic-related, it could be a crazy ride in the meantime.

Read more stories on the economy:

44m agoItem 1 of 6

Most policymakers believe that today’s rapid inflation will fade. But there is a danger that the global price surge could last longer — and become more country-specific — if workers in nations experiencing high inflation today bargain for wage increases and are more accepting of steadily higher prices. Bringing entrenched inflation back under control could require painful monetary policy responses, ones that would probably plunge national economies back into recession.

If inflation does fade as policymakers expect, the current burst could actually offer benefits. READ THE ARTICLE →

John C. Williams, the president of the Federal Reserve Bank of New York and a powerful monetary policy official, hinted that it might be possible for the central bank to begin removing support for the economy before the end of the year even if the job market grows at a lackluster pace in coming months.

The Fed has been buying $120 billion in government-backed bonds each month to help the economy by keeping interest rates low and money flowing. Policymakers have been debating when to begin slowing that program. They said in December that they would do so only once they had made “substantial further progress” toward maximum employment and inflation that averages 2 percent over time.

Key policymakers have made it clear that the inflation side of that goal has been satisfied, with prices up markedly this year, but they have been waiting for more progress on employment. Assessing the job market has been complicated by surging coronavirus infections tied to the Delta variant, and payroll gains slowed in August.

Mr. Williams, who holds a constant vote on monetary policy and is foremost among the central bank’s 12 regional policymakers, told reporters on Wednesday that he had been looking at the cumulative level of employment progress rather than month-to-month changes — suggesting that weakening jobs growth would not necessarily make impossible a start to the so-called taper.

“It’s not a speed condition,” Mr. Williams said. “It’s really about, where are we, relative, on this path back toward maximum employment?”

He added that he was looking not just at job gains but also at measures like labor force participation for a “full picture” of how much progress the job market has made.

“Some months come in stronger, some not so strong,” Mr. Williams said. “It’s really about accumulation.”

He added, “We’ll have to wait and see the data as it comes in.”

Mr. Williams said during a speech earlier in the day that if the economy continued to improve as he expected, “it could be appropriate to start reducing the pace of asset purchases this year.” Pulling back on bond buying will be just a first step in removing support, and the Fed’s policy interest rate is expected to remain at near zero for some time.

His comments came just as the Fed released its latest anecdotal survey of business contacts across its regional districts, commonly called the “Beige Book.” “Delta” was referenced 32 times as employers reported that “growth downshifted slightly to a moderate pace in early July through August.”

Read moreRelated reporting

More World News →

Paul Biya’s Re-Election: What Cameroon’s Political Longevity Reveals About Leadership and Governance in Africa

From Power to Prison: The Fall of France’s Former President Nicolas Sarkozy

The War in Ukraine: A Comprehensive Analysis of the Conflict